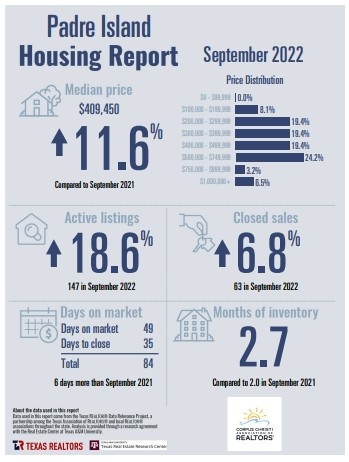

The Local Real Estate Market active listing median prices have risen to $409,450 this past month compared to last September at this time!

Corpus Christi Association of Realtors continues to show us the data that shows prices up 11.6% in median price homes while inventory Has been rising 2.7 compared to 2.0 last year during the month of September.

Days on the market for sale have risen to an average of 49 days on the market and the highest category for sales with 24.2% of all the sales was priced between $500,000 – $749,999. The market is stable but cooling off quite a bit now as we head toward the holidays, we are keeping our eyes on those mortgage rates and whether the FED will raise benchmark interest rates in their November 2022 meeting.

Many of us brokers have seen it all before, Coastline has been weathering the conditions of different markets since 1995. Our market is very unique and the word over the bridge and up North is “Padre Island is on the move.” There is more dirt turning on our little sandbar right now than we have seen in decades, exciting times ahead for residents.

Cheri Sperling is the owner of Coastline Properties with a dedicated team of agents specializing in residential listings, sales, and property management in the Padre Island real estate market. Coastline’s team is the most knowledgeable real estate office on Padre Island. No pressure style, patience, and an intimate understanding of the local market. They go to work for you!

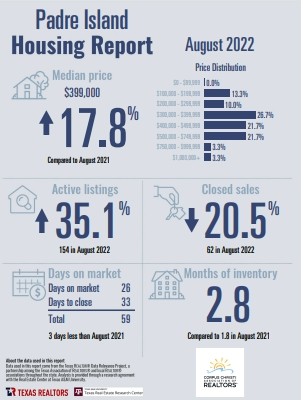

Padre Island September 2022 Data (Click Pic below for Larger Image)

Helter swelter, you could fry an egg on the sidewalk! Eat the egg, but don’t BE the egg. If you follow these 10 tips, you may actually find that there are ways to enjoy the dog days of summer. Our bodies, moods, and bills take a toll during the scorching summer heat, but don’t let the temperature and humidity keep you from the beach, outdoor entertaining, and boating. Stay cool, my comPADREs.

Helter swelter, you could fry an egg on the sidewalk! Eat the egg, but don’t BE the egg. If you follow these 10 tips, you may actually find that there are ways to enjoy the dog days of summer. Our bodies, moods, and bills take a toll during the scorching summer heat, but don’t let the temperature and humidity keep you from the beach, outdoor entertaining, and boating. Stay cool, my comPADREs.