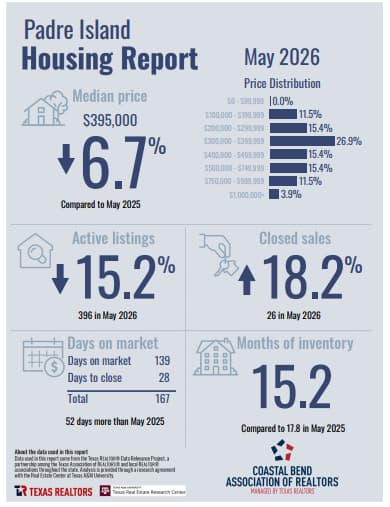

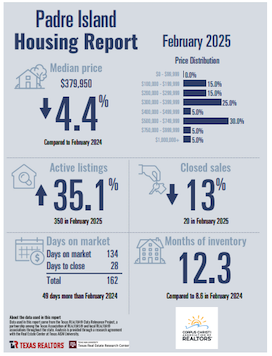

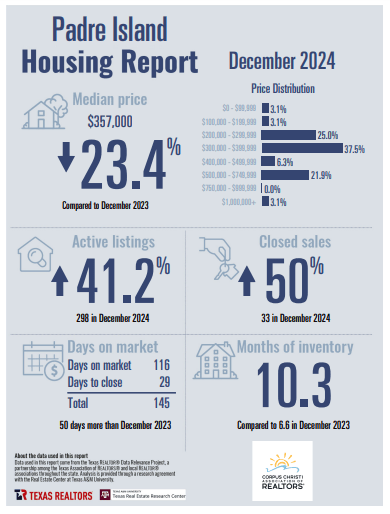

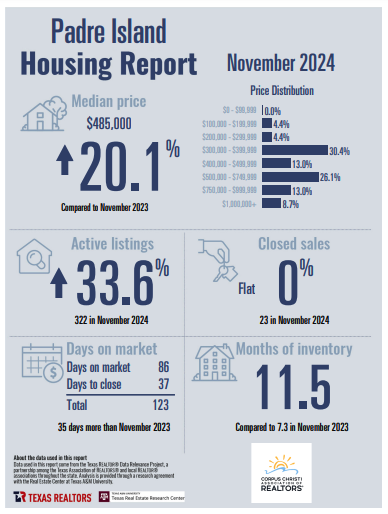

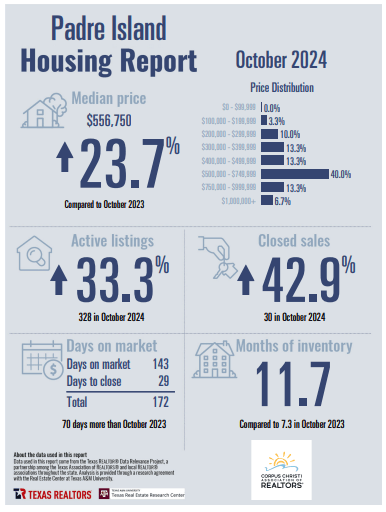

Corpus Christi Association of Realtors has posted the Padre Island Corpus Christi Housing Report for May 2026.

May 2026 continues to show a market that is finding balance while maintaining strong long term value on Padre Island.

The median home price in May was $395,000, down 6.7% from May 2025. While prices softened compared to last year, buyer activity improved. Closed sales increased 18.2%, with 26 homes sold compared to 22 during the same month last year. That increase in transactions suggests buyers are responding to improved affordability and greater opportunities in the market.

Inventory remains elevated, but it is moving in a positive direction. Months of inventory declined from 17.8 months last May to 15.2 months today. Active listings also decreased 15.2% year over year, falling to 396 homes on the market. Those trends indicate excess inventory is gradually being absorbed.

Homes are still taking longer to sell, averaging 167 days from listing to closing, which is 52 days longer than a year ago. Even so, market times improved from April, and the increase in closed sales suggests motivated buyers are continuing to make purchasing decisions.

One of the most interesting data points is where buyers are purchasing. The largest share of sales occurred in the $300,000 to $399,999 price range, accounting for 26.9% of all homes sold during May. This was the strongest performing price category on Padre Island, highlighting continued demand for moderately priced island properties that offer both lifestyle and value.

Taken together, the May numbers paint an encouraging picture. Buyers have more choices and negotiating power than they have had in years, while sellers continue to benefit from a market that remains active. With inventory trending lower, sales activity rising, and the strongest demand centered in the mid market price range, Padre Island appears to be entering the summer season with growing momentum and a healthier balance between buyers and sellers than we saw a year ago. May’s Consumer Price Index rose 4.2% from a year earlier, largely due to higher energy costs. Despite the increase, core inflation remained below 3%, which could help support housing demand if mortgage rates remain stable during the busy summer buying season.

Padre Island’s newest development Whitecap NPI is open for sales of their lots in Phase 1, Contact Coastline Properties owner Cheri Sperling for all pre-sales. sperling@coastline-properties.com

Cheri Sperling is the owner of Coastline Properties with a dedicated team of agents specializing in residential listings, sales, and property management in the Padre Island Corpus Christi real estate market. Coastline’s team is the most knowledgeable real estate office on Padre Island. No pressure style, patience, and an intimate understanding of the local market. They go to work for you!

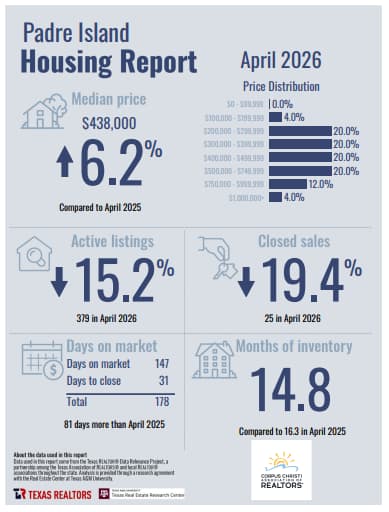

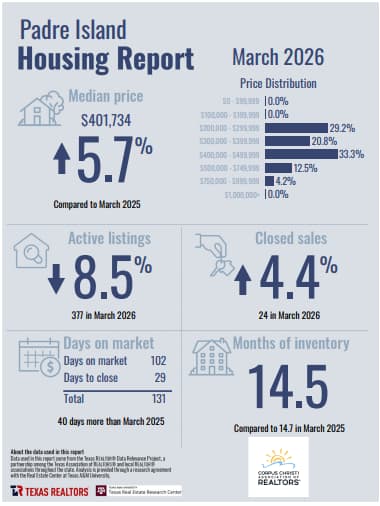

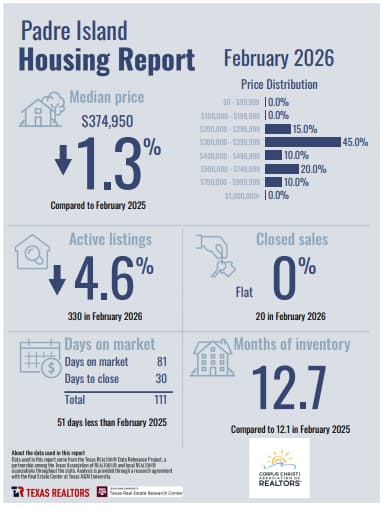

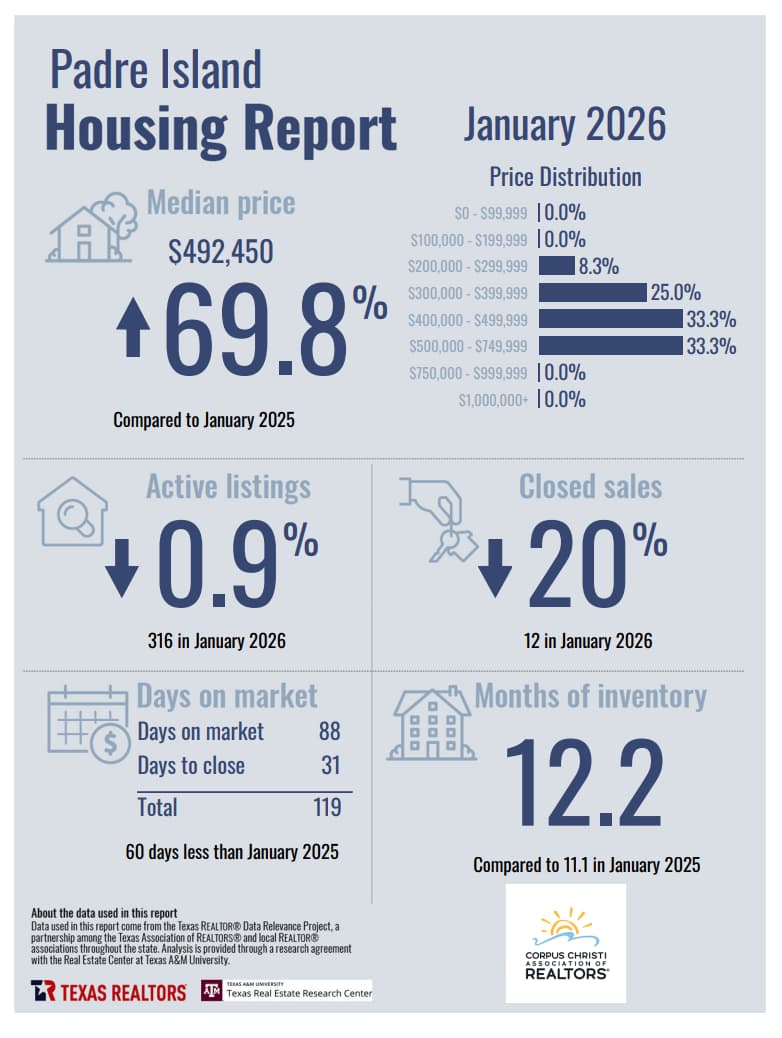

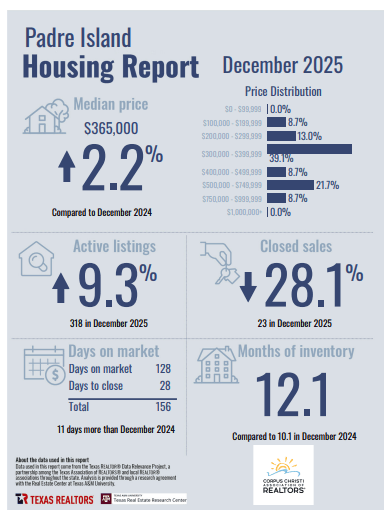

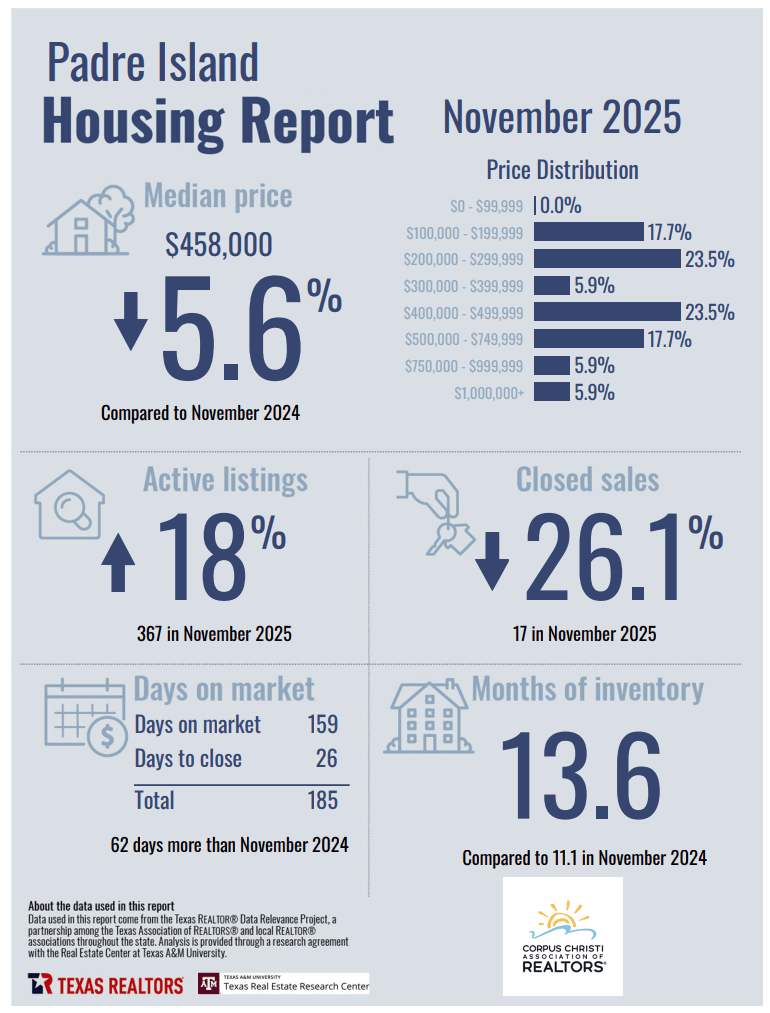

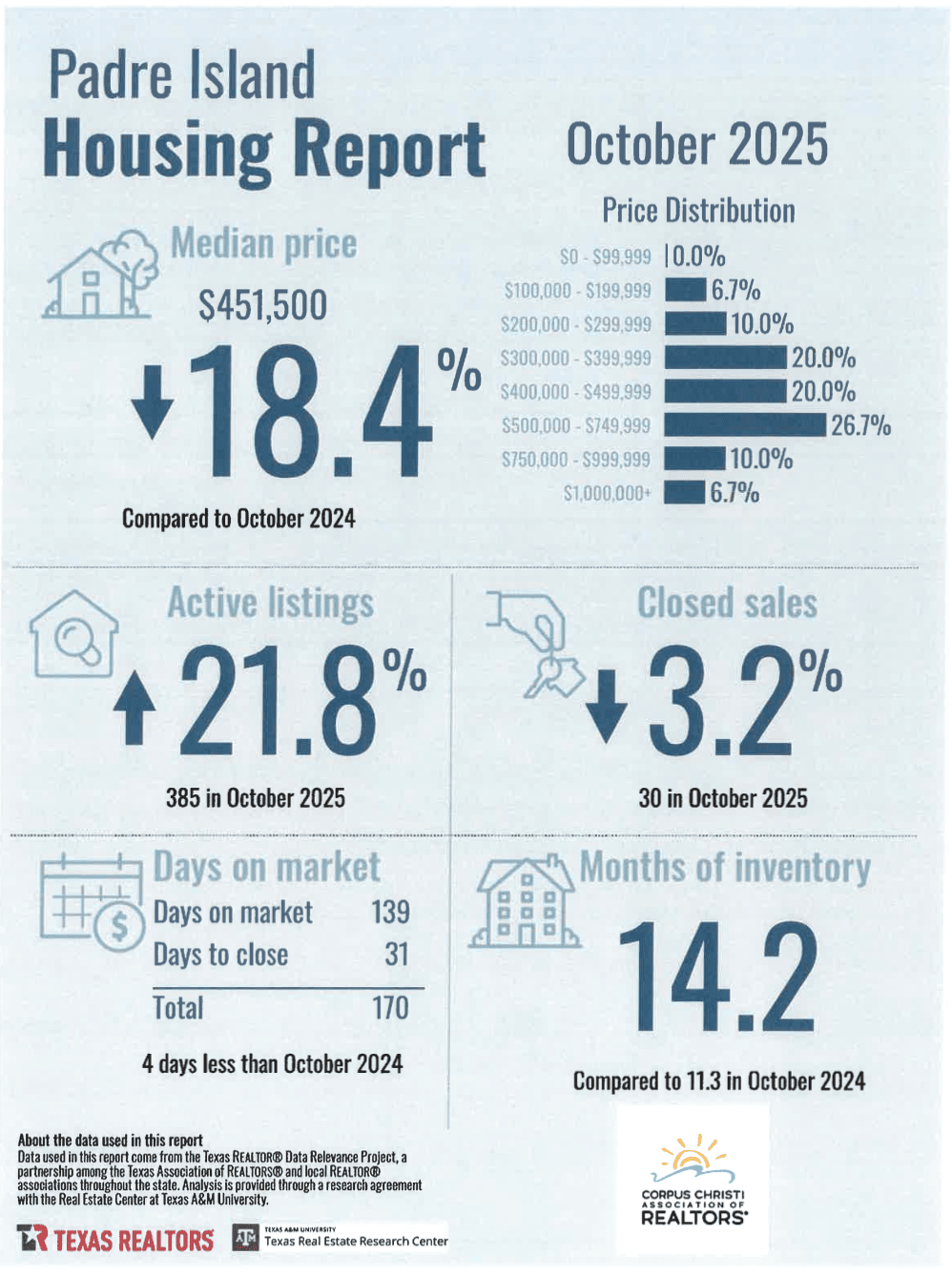

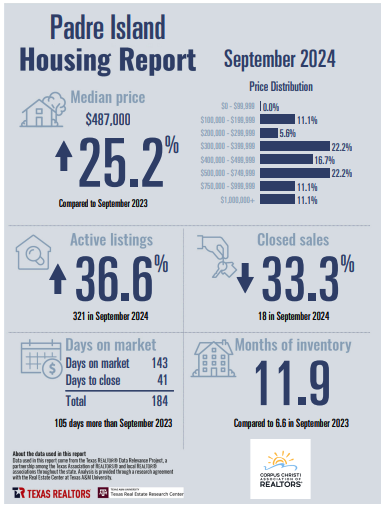

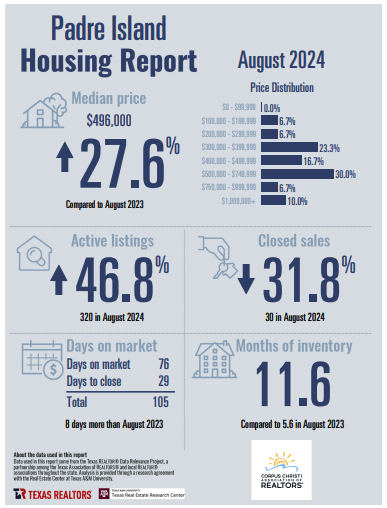

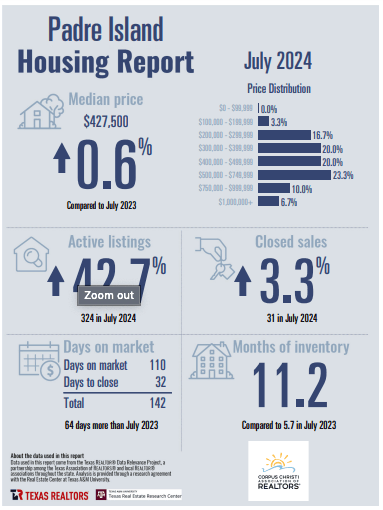

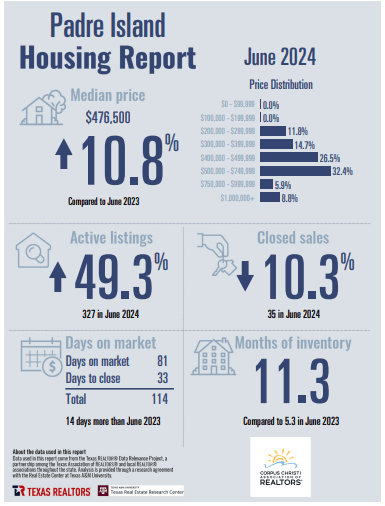

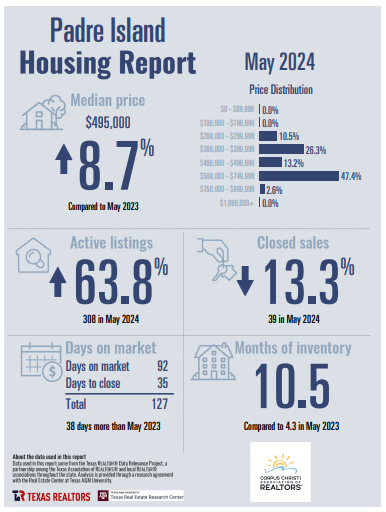

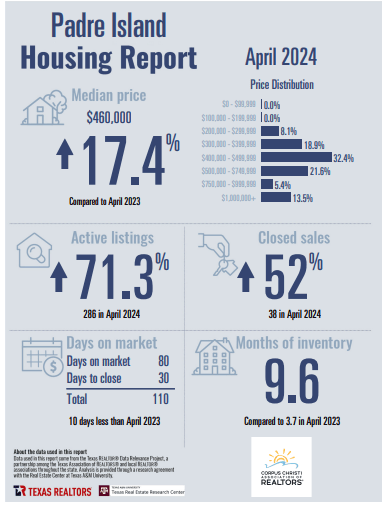

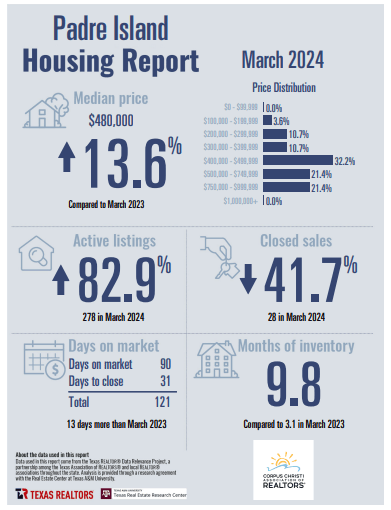

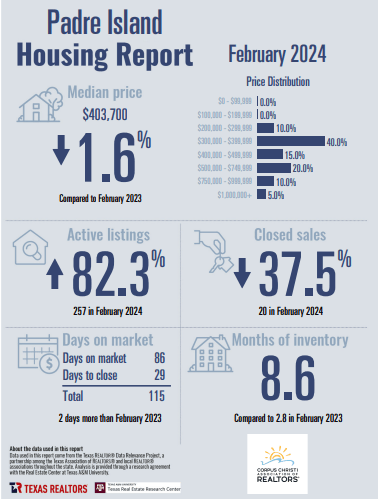

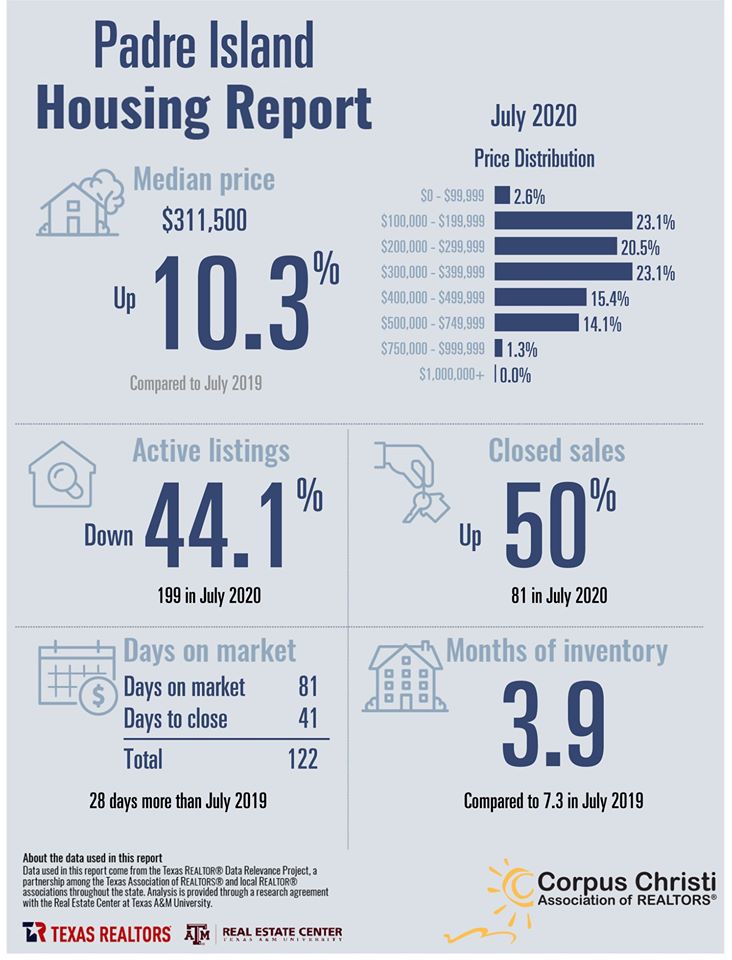

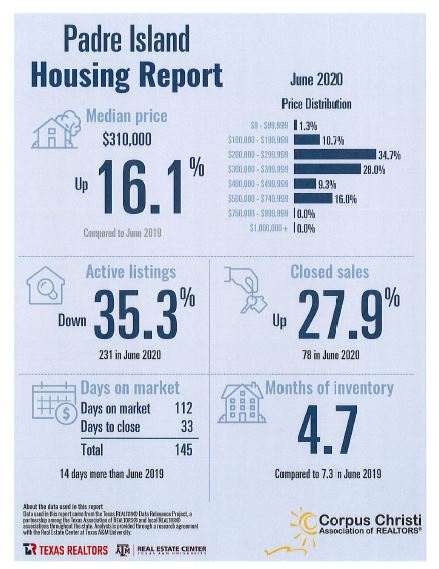

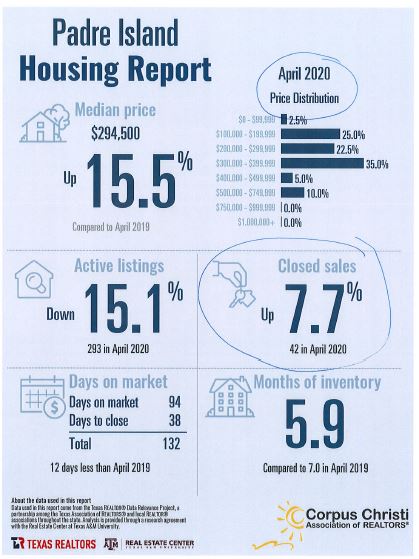

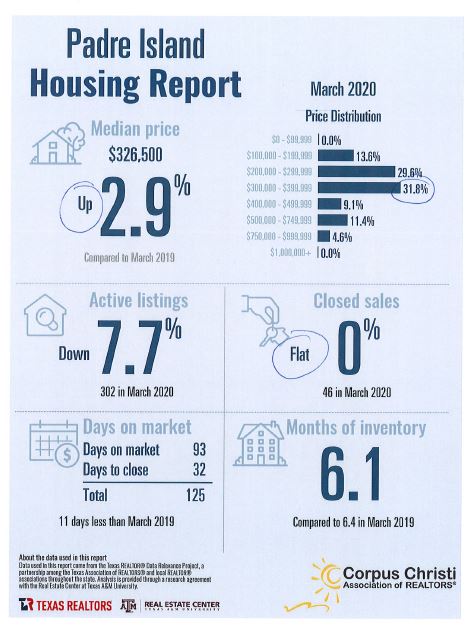

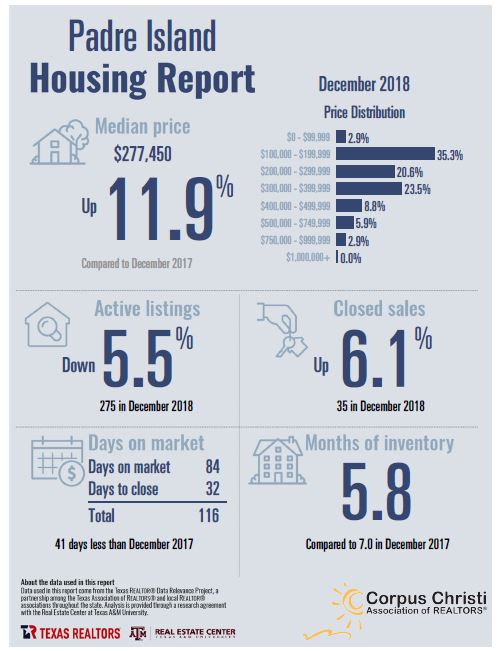

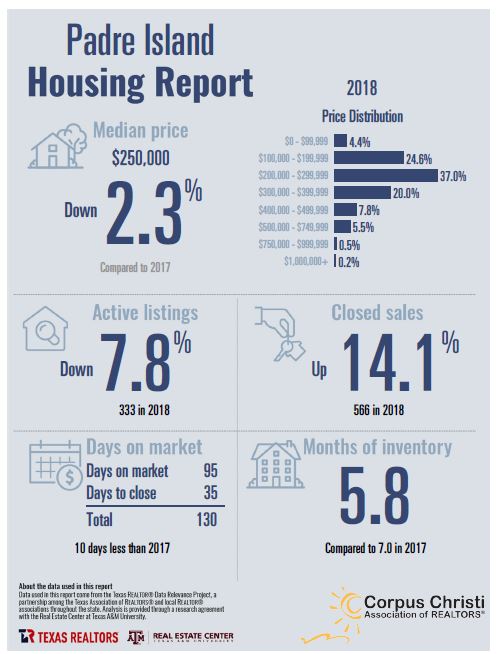

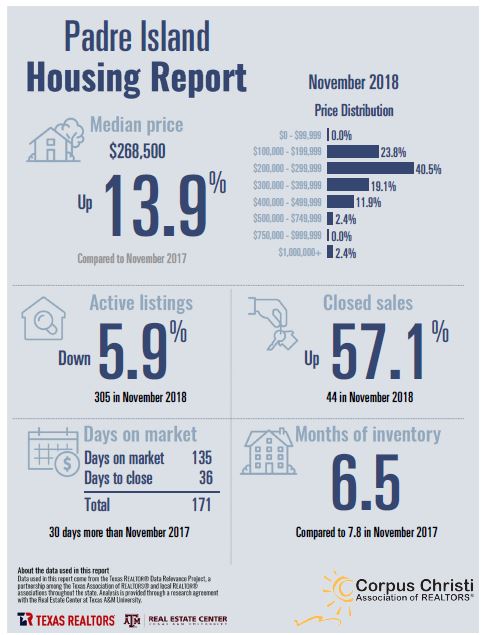

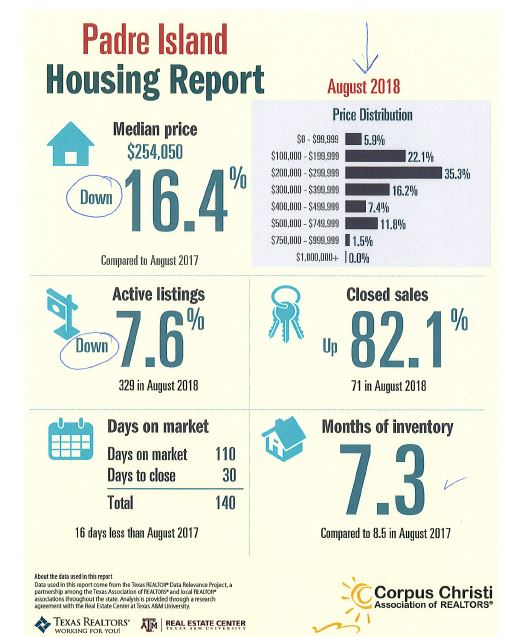

Padre Island Corpus Christi May 2026 Data (Click Pic below for Larger Image)

As we enter 2026, the island and the greater Corpus Christi area are gearing up for another successful tourism season, with several city efforts focused on enhancing the visitor experience while supporting local businesses and residents alike. With Spring Break and summer on the horizon, the City proactively launches beach maintenance, park improvements, and business-friendly policies aimed at keeping our coastal community welcoming and safe.

As we enter 2026, the island and the greater Corpus Christi area are gearing up for another successful tourism season, with several city efforts focused on enhancing the visitor experience while supporting local businesses and residents alike. With Spring Break and summer on the horizon, the City proactively launches beach maintenance, park improvements, and business-friendly policies aimed at keeping our coastal community welcoming and safe.

I, for one, admire Winter Texans. They’ve got the right idea: Come to our piece of paradise, spend a few months, spend a few bucks, then repeat! Some come in RVs, others have a home/townhome/condo to which they retreat. The time is coming to welcome our Winter Texans back, and it’s the Winter Texan “way” that reminds me of one powerful investment tool – real estate of course! We are lucky enough to live in a place where many come to vacation. Whether you live here and want to capitalize on the growing rental market, or you’ve got relatives and friends to whom you’d love to persuade to do the same or invest in a vacation home…Get your own piece of Padre Island Pie!

I, for one, admire Winter Texans. They’ve got the right idea: Come to our piece of paradise, spend a few months, spend a few bucks, then repeat! Some come in RVs, others have a home/townhome/condo to which they retreat. The time is coming to welcome our Winter Texans back, and it’s the Winter Texan “way” that reminds me of one powerful investment tool – real estate of course! We are lucky enough to live in a place where many come to vacation. Whether you live here and want to capitalize on the growing rental market, or you’ve got relatives and friends to whom you’d love to persuade to do the same or invest in a vacation home…Get your own piece of Padre Island Pie!

It’s hot here on Padre Island, and I’m not talking just the high temperatures. It is real estate’s steamy season, and properties are being listed and sold faster than season tickets at the ‘bahn. With the active market, it’s critical to take a look at your spending. How can you be assured you’re not wasting money? Here are some smart tips on how to save and spend during peak purchase season. Do not fall victim to these common money mistakes.

It’s hot here on Padre Island, and I’m not talking just the high temperatures. It is real estate’s steamy season, and properties are being listed and sold faster than season tickets at the ‘bahn. With the active market, it’s critical to take a look at your spending. How can you be assured you’re not wasting money? Here are some smart tips on how to save and spend during peak purchase season. Do not fall victim to these common money mistakes.

Here is our top 6 tips for the New Year

Here is our top 6 tips for the New Year

With the flooding and other tragedies that have occurred across the state, it is important that consumers be aware of Chapter 57 of the Texas Business and Commerce Code that was enacted by HB 1711 effective September 1, 2011. The bill applies to contractors who remove, clean, sanitize, demolish, reconstruct, or otherwise treat improvements to real property as a result of damage or destruction to that property caused by a natural disaster. Specifically, it requires that a “disaster remediation” contract must be in writing and prohibits a “disaster remediation contractor” from requiring payment prior to beginning work or charging a partial payment in any amount disproportionate to the work that has been performed. However, the statute exempts contractors that have held a business address for at least one year in the county or adjacent county where the work occurs.

With the flooding and other tragedies that have occurred across the state, it is important that consumers be aware of Chapter 57 of the Texas Business and Commerce Code that was enacted by HB 1711 effective September 1, 2011. The bill applies to contractors who remove, clean, sanitize, demolish, reconstruct, or otherwise treat improvements to real property as a result of damage or destruction to that property caused by a natural disaster. Specifically, it requires that a “disaster remediation” contract must be in writing and prohibits a “disaster remediation contractor” from requiring payment prior to beginning work or charging a partial payment in any amount disproportionate to the work that has been performed. However, the statute exempts contractors that have held a business address for at least one year in the county or adjacent county where the work occurs.

It’s no secret that it costs a lot to live on the coast, especially once you add up your taxes, homeowner’s insurance, flood insurance, and windstorm insurance. And in 2012, the Texas Department of Insurance (TDI) proceeded forward with several proposals to fund the Texas Windstorm Insurance Association (TWIA), the provider of last resort for windstorm insurance on our coast. It was then that TWIA adopted a 5% increase on all residential and commercial windstorm insurance policies to policyholders in the 14 counties (Aransas, Brazoria, Calhoun, Cameron, Chambers, Galveston, Jefferson, Kenedy, Kleberg, Matagorda, Nueces, Refugio, San Patricio, and Willacy) comprising the Texas Coast. This was the third rate increase since 2009. But the long fight is finally over.

It’s no secret that it costs a lot to live on the coast, especially once you add up your taxes, homeowner’s insurance, flood insurance, and windstorm insurance. And in 2012, the Texas Department of Insurance (TDI) proceeded forward with several proposals to fund the Texas Windstorm Insurance Association (TWIA), the provider of last resort for windstorm insurance on our coast. It was then that TWIA adopted a 5% increase on all residential and commercial windstorm insurance policies to policyholders in the 14 counties (Aransas, Brazoria, Calhoun, Cameron, Chambers, Galveston, Jefferson, Kenedy, Kleberg, Matagorda, Nueces, Refugio, San Patricio, and Willacy) comprising the Texas Coast. This was the third rate increase since 2009. But the long fight is finally over.